Paytm’s could be the largest IPO debut in India in a year that will see Zomato, CarTrade and others also go public

According to research firm AllianceBernstein’s pre-IPO primer for Paytm, the company has shown financial discipline which is rare in the hyper-competitive payments space

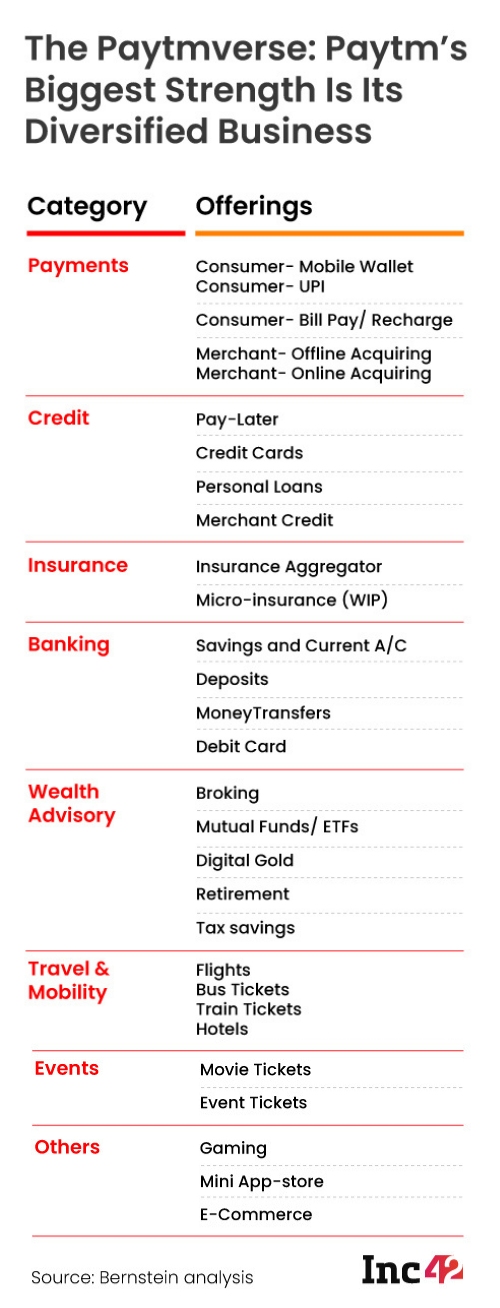

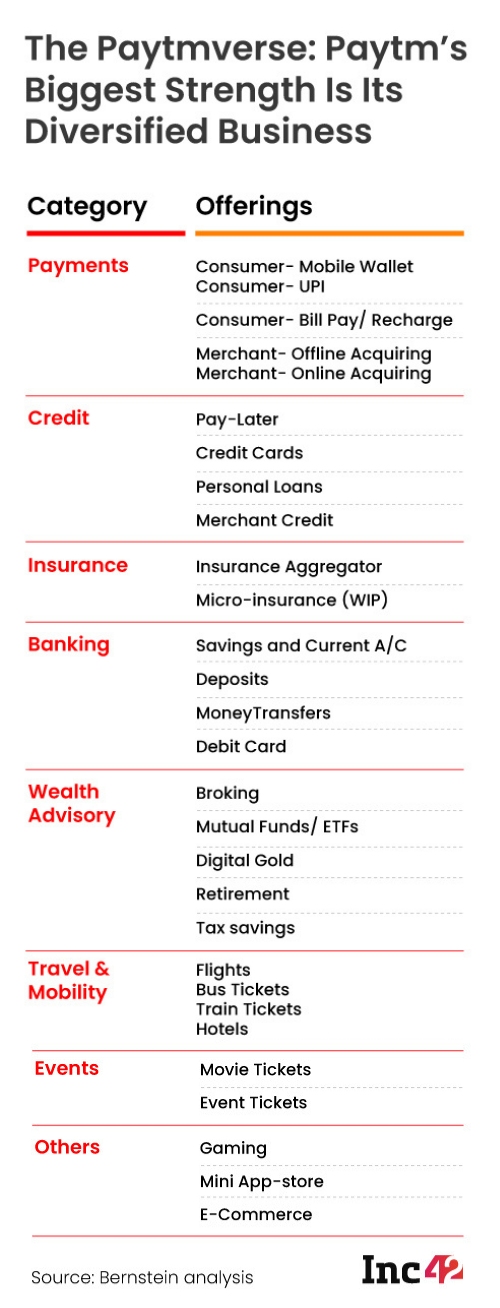

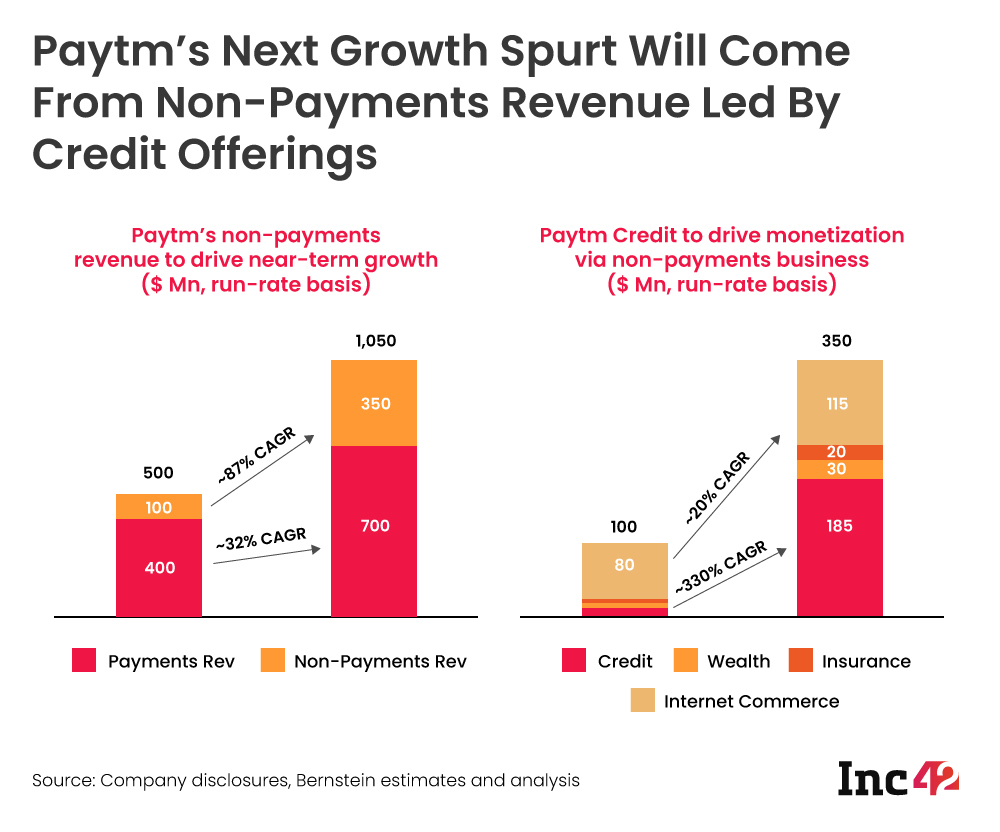

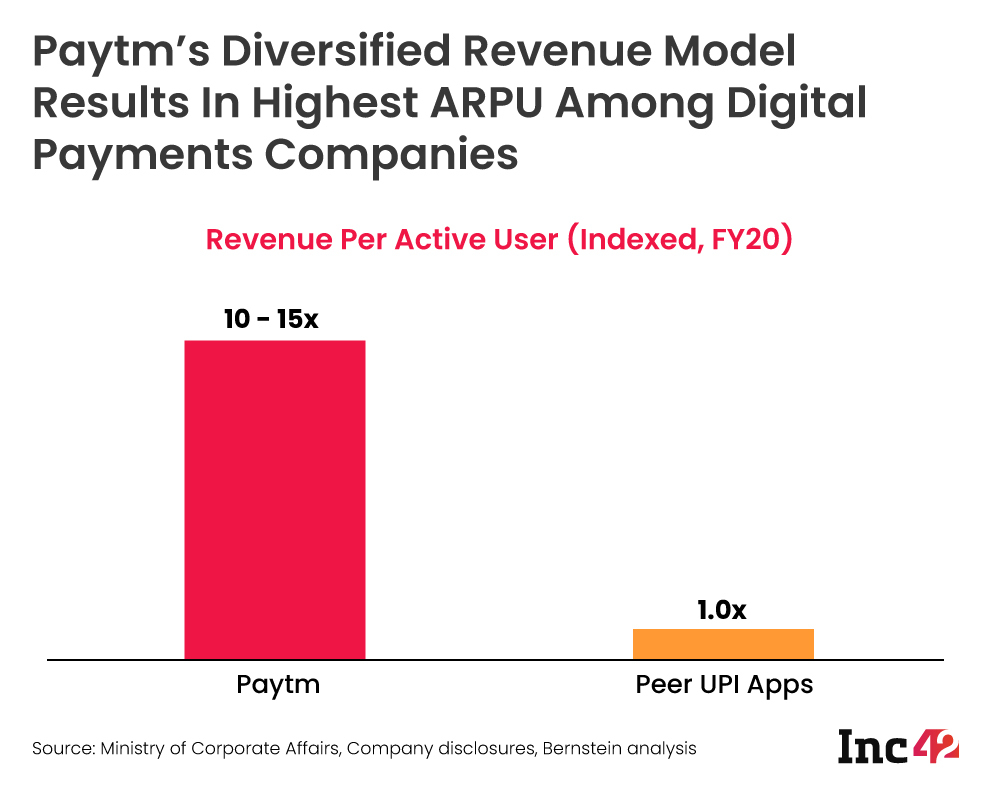

Besides this, Paytm’s diversified revenue and business model is being seen as a big advantage against the competition

Digital payments giant Paytm, operated by One97 Communications, is planning to raise INR 21,800 Cr ($3 Bn) in an initial public offering (IPO) by November this year. The Vijay Shekhar Sharma-led company is targeting a valuation of $25 Bn – $30 Bn, a big jump from its current $16 Bn valuation.

Paytm could be the largest IPO debut in India in a year in which food aggregator Zomato and used cars marketplace CarTrade, epharmacy startup PharmEasy, beauty ecommerce brand Nykaa and insurtech startup PolicyBazaar are likely to list publicly.

Paytm’s much-anticipated public market debut will include a mix of new and existing shares to meet regulatory obligations in India, and offer partial exit to some existing backers. The company has shortlisted Morgan Stanley, Citigroup Inc and JPMorgan Chase & Co as advisors for this IPO, with Morgan Stanley as the top contender. The IPO process is expected to start from late June or early July onwards, as per reports.

Founded in 2000 by Vijay Shekar Sharma, One97 Communications started out as a prepaid and mobile recharge platform before Paytm was launched in 2010. Paytm is today one of the biggest digital payments companies in India with its offering spread across digital payments like UPI, credit and debit cards, wealth management through Paytm Money, banking services through Paytm Payments Bank and more.

Diversification Could Be The Key To Paytm’s Successful IPO

According to research firm AllianceBernstein’s pre-IPO primer for Paytm, which has been reviewed by Inc42, the company has shown financial discipline which is rare in the hyper-competitive payments space. Paytm is said to be on track to break even in 12-18 months and the research report expects Paytm to lead the payments and fintech market because of its diversification.

One97 Communications operates Paytm Payments Bank Limited, Paytm General Insurance Limited, Paytm Life Insurance Limited, Paytm Money Limited, Paytm E-Commerce Private Limited, Paytm Entertainment Limited among other smaller entities. These combine to give Paytm a strong acquisition channel for its core business of payments and fintech services.

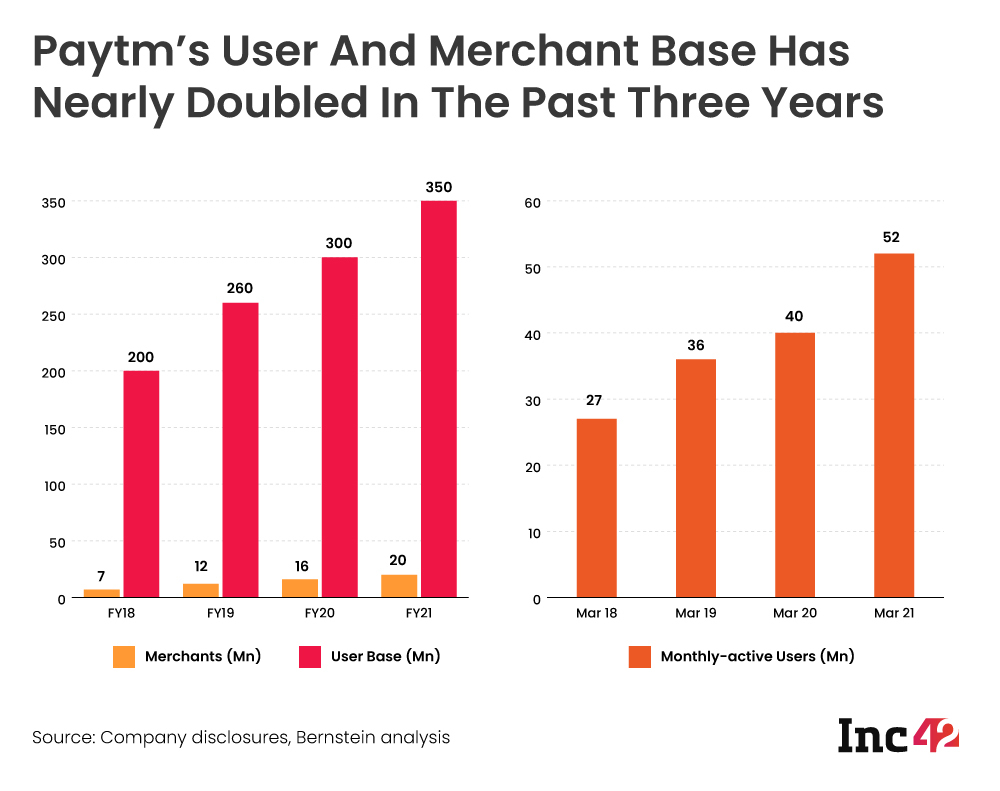

Leading Among Payments Rivals

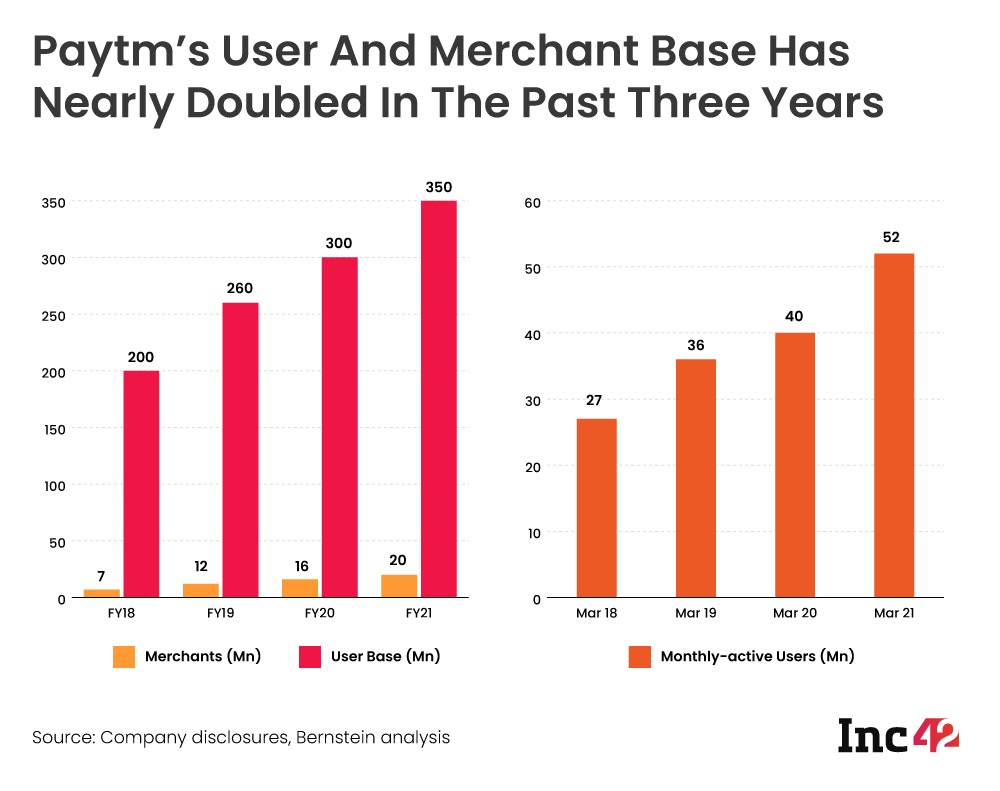

The company has over 350 Mn users overall with 50 Mn monthly active users and 20 Mn+ merchants, according to Bernstein’s primer. Beside this, it has processed over 1.2 Bn monthly transactions across offline and online payments as well as financial services in February 2021.

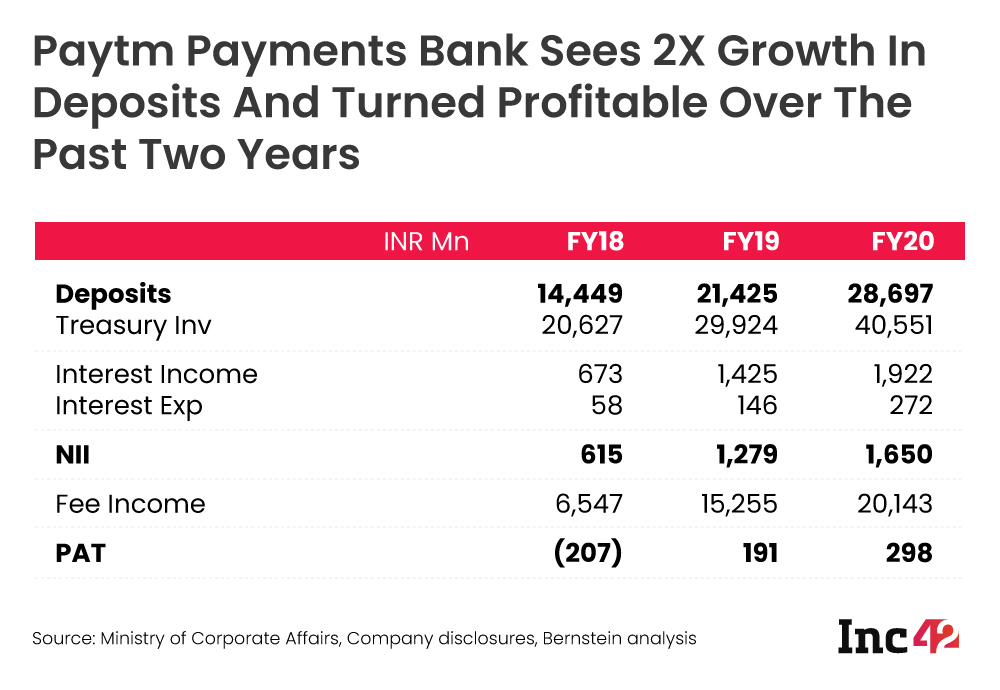

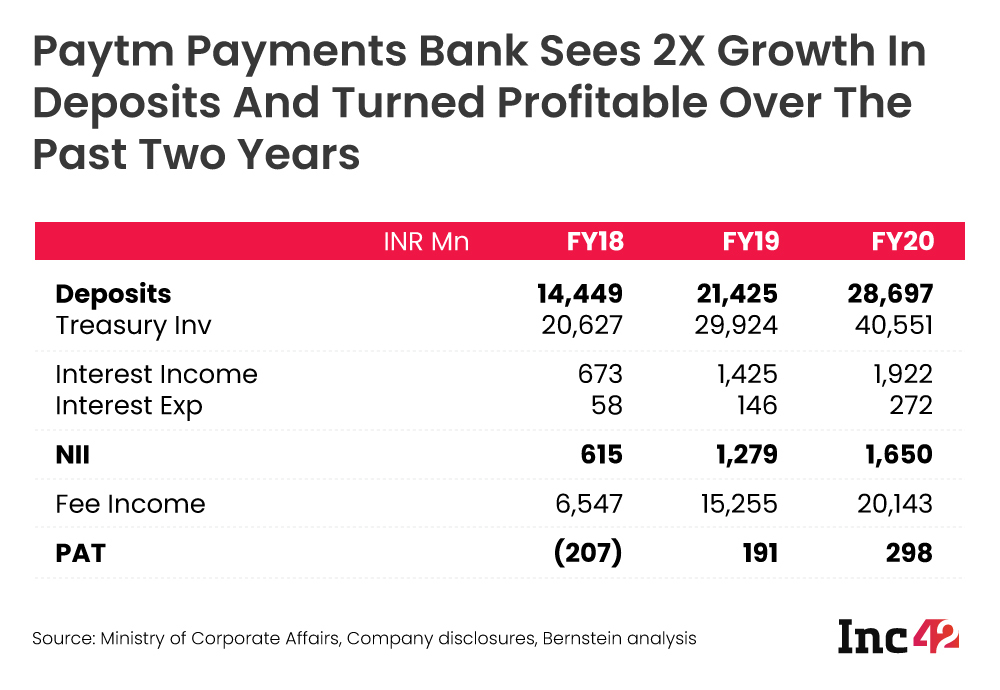

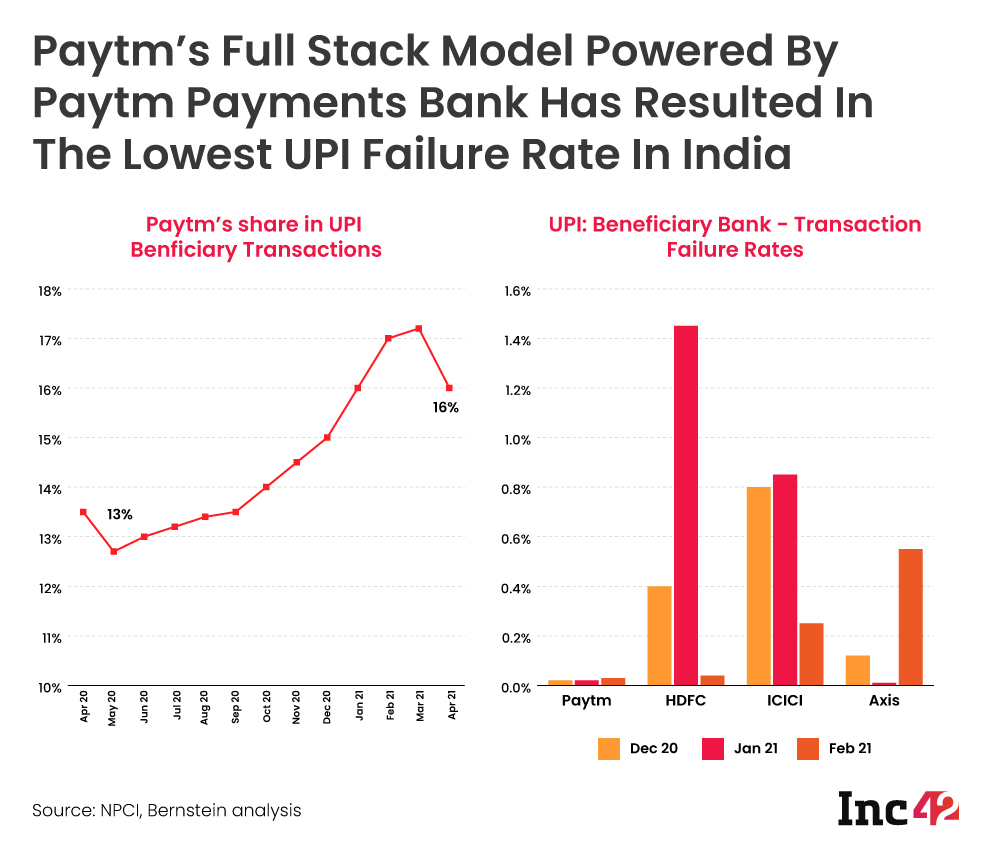

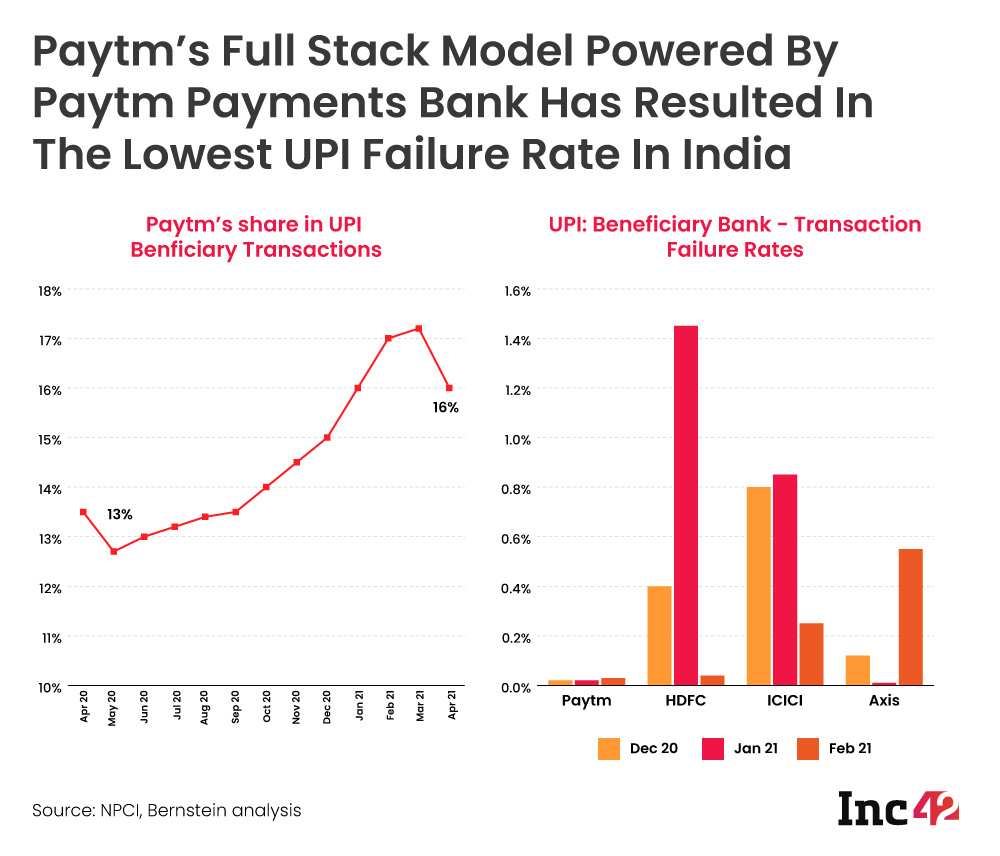

Paytm Payments Bank also achieved an all-time high monthly target by opening over 1 Mn new savings and current accounts in March 2021, with the total number of bank accounts going up to 64 Mn. It also led the beneficiary banks on UPI platform, by processing 469.8 Mn transactions in March and 430.04 Mn in April. This allows Paytm to have a wide base from which to earn revenue.

Paytm Payments Bank also achieved an all-time high monthly target by opening over 1 Mn new savings and current accounts in March 2021, with the total number of bank accounts going up to 64 Mn. It also led the beneficiary banks on UPI platform, by processing 469.8 Mn transactions in March and 430.04 Mn in April. This allows Paytm to have a wide base from which to earn revenue.

Not Just About UPI

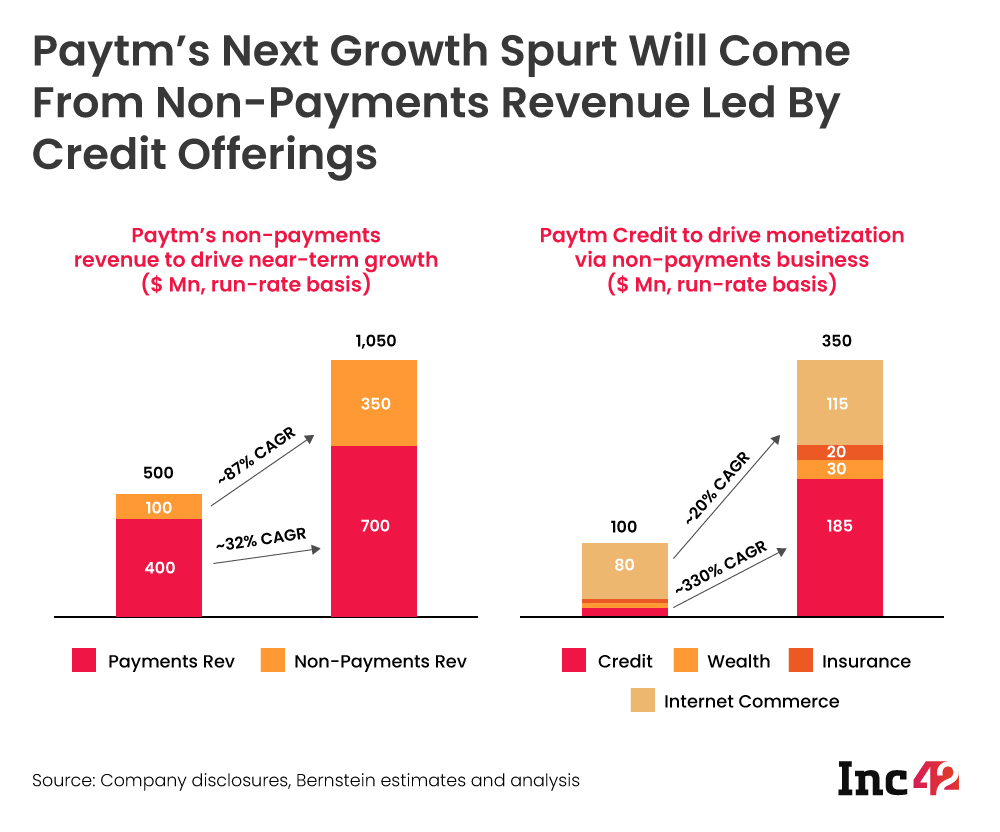

Among the key strengths for Paytm is its relatively lower dependence on UPI payments for growth or revenue. Bernstein notes that maintaining UPI market share requires a lot of marketing spending with no real revenue coming back. This has been seen in our in-depth analysis of the UPI payments sector as well, which is why other players are also looking to diversify like Paytm has done in the past 10 years. So instead of focussing on UPI, Paytm has built up its more revenue-friendly merchant payments solutions, as well as other services such as Paytm Payouts for business payroll, Paytm Money, insurance, credit and more.

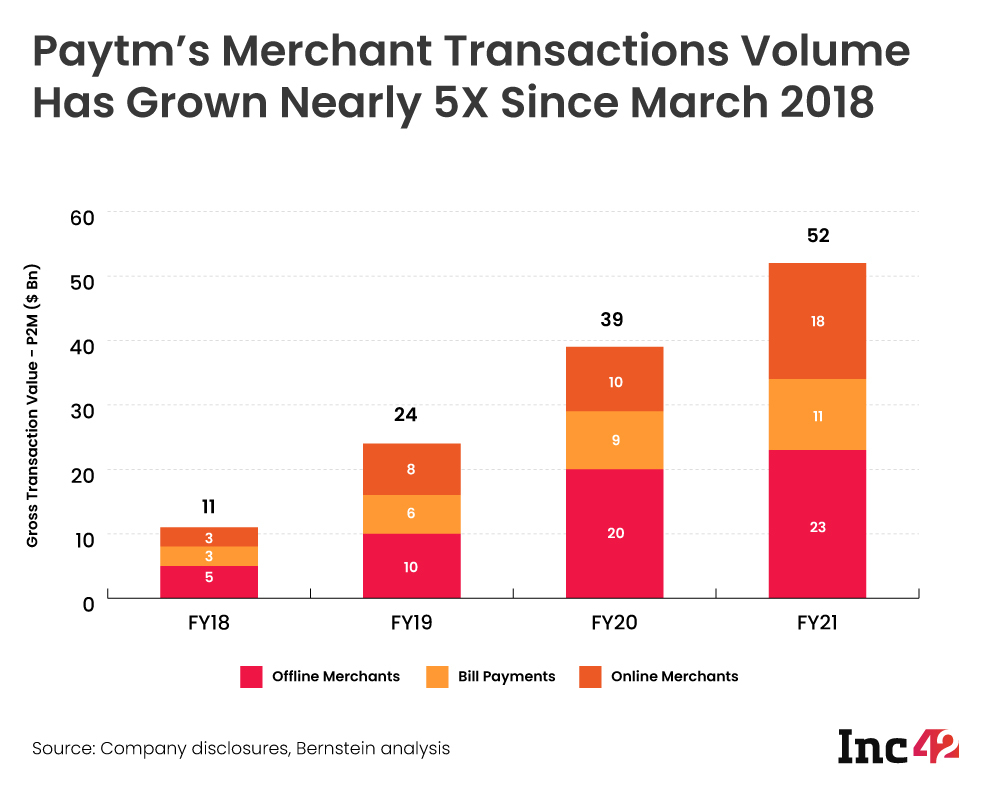

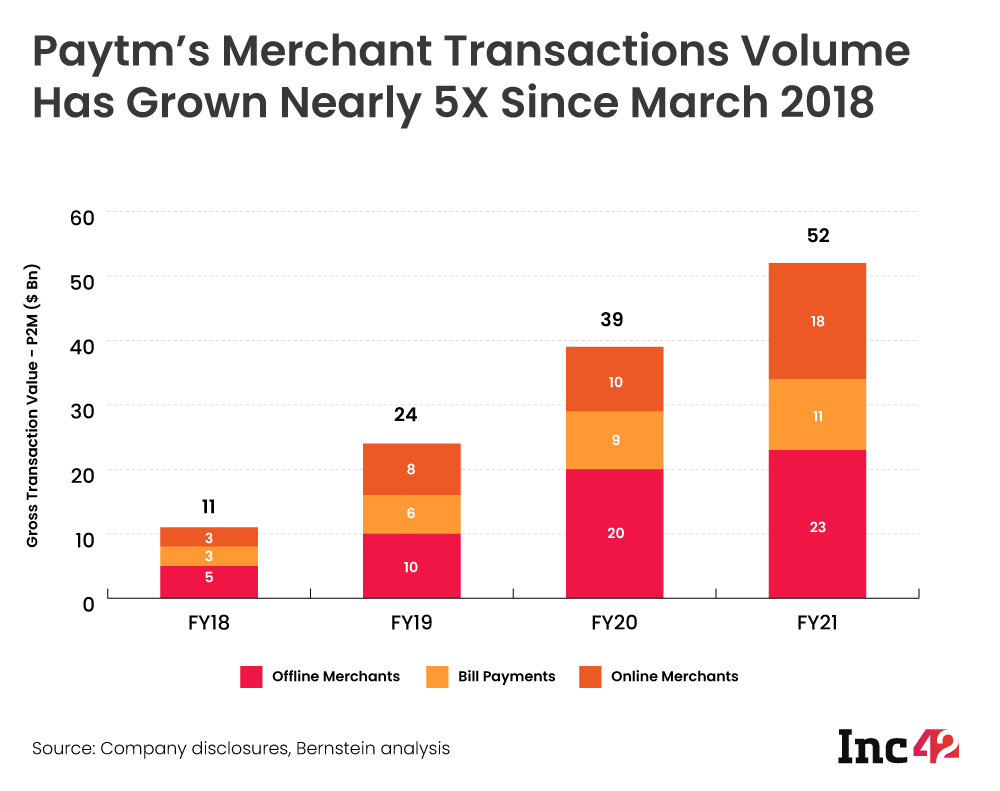

Merchant Payments Focus Paying Off

Outside of UPI, Paytm has decided to focus on services and solutions that cater to the merchant class that need to digitise their payments.

The focus on merchants has also enabled Paytm Payments Bank (PPB) to lead the market when it comes to beneficiary bank market share in UPI payments. Paytm has managed to keep its lead in this regard by offering the full stack for UPI payments by owning the issuing and beneficiary bank i.e PPB as well as the UPI app, unlike the two leading UPI apps Google Pay and PhonePe, which rely on third-party banks. This is most evident in the lower failure rate for Paytm when compared to the competition.

Unlike independent merchant acquirers who have to work with partner banks, Paytm’s merchant acquiring is integrated with Paytm Payments Bank. This creates a seamless integration layer and this same advantage extends to UPI and online payments.

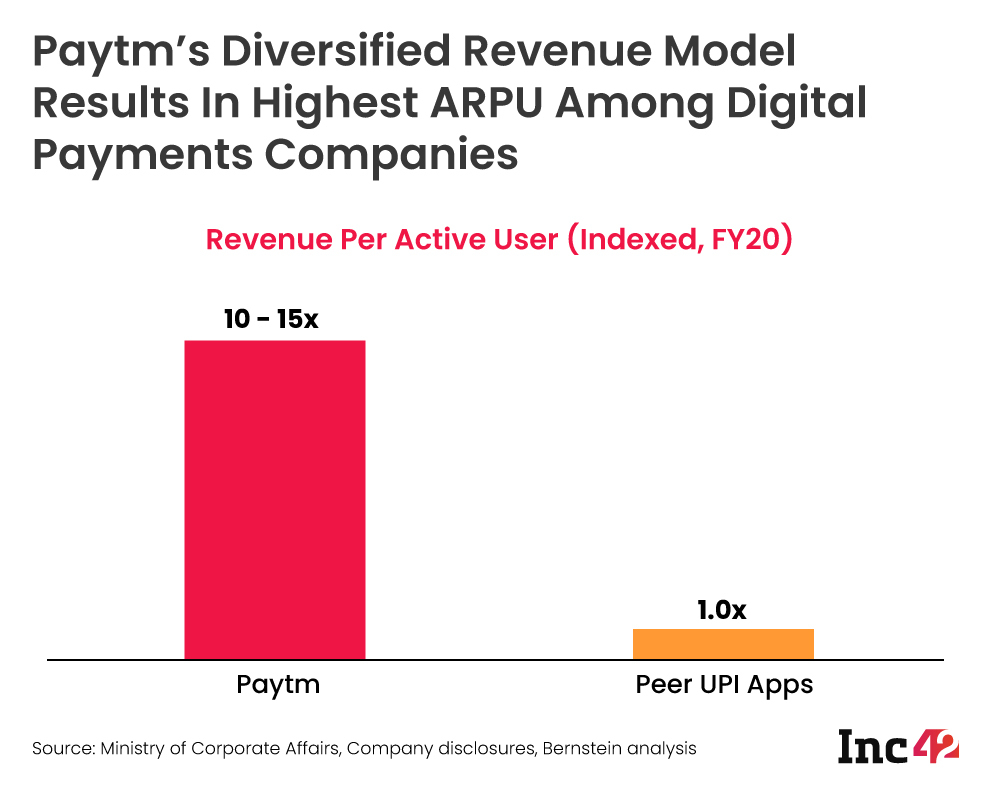

Further, the diversified business with merchant-focussed services, Paytm Money, Paytm Insurance, Paytm Postpaid has directly resulted in higher ARPU for Paytm compared to the competition.

In fact, Paytm’s non-payment revenue has grown steadily on the back of its buy now pay later (BNPL) credit product Paytm Postpaid, short-term personal loans and credit card services, as well as the commissions it earns from retail investors on the Paytm Money investment app and through Paytm Insurance.

Currently, Paytm’s payments bank license means that it cannot disburse loans from its own books and has to use a banking partner.

Can Paytm Extend Its Lead Over Fintech Rivals?

A key future objective for Paytm would be getting the small finance bank license, which would allow it to build a universal bank with a strong digital edge backed by fully digital onboarding and customer servicing on the app.

However, other companies are looking at more diversified services too. Walmart-owned PhonePe, which is also planning to launch an IPO by 2023 as per reports, has looked to move beyond the broken revenue model on the UPI. PhonePe has entered a few lucrative segments and tested the waters. After Flipkart’s acquisition by Walmart, the PSP registered three more entities with the Ministry of Corporate Affairs (MCA). These include PhonePe Wealth Services (a mutual fund distributor), PhonePe Insurance Broking (a third-party insurance distributor) and PhonePe Technology Services.

Besides Paytm, Sachin Bansal-owned Navi Technologies is another rival for Paytm and the company is also looking for a universal banking license, having adopted an acquisition strategy to enter the financial services arena.

Compared to the competition though, Paytm’s full-stack service suite is similar to neobanking startups in the West such as Chime, N26, NuBank, according to Bernstein, thanks to the tight integration between its various aspects, that its fintech rivals in India cannot match just yet.