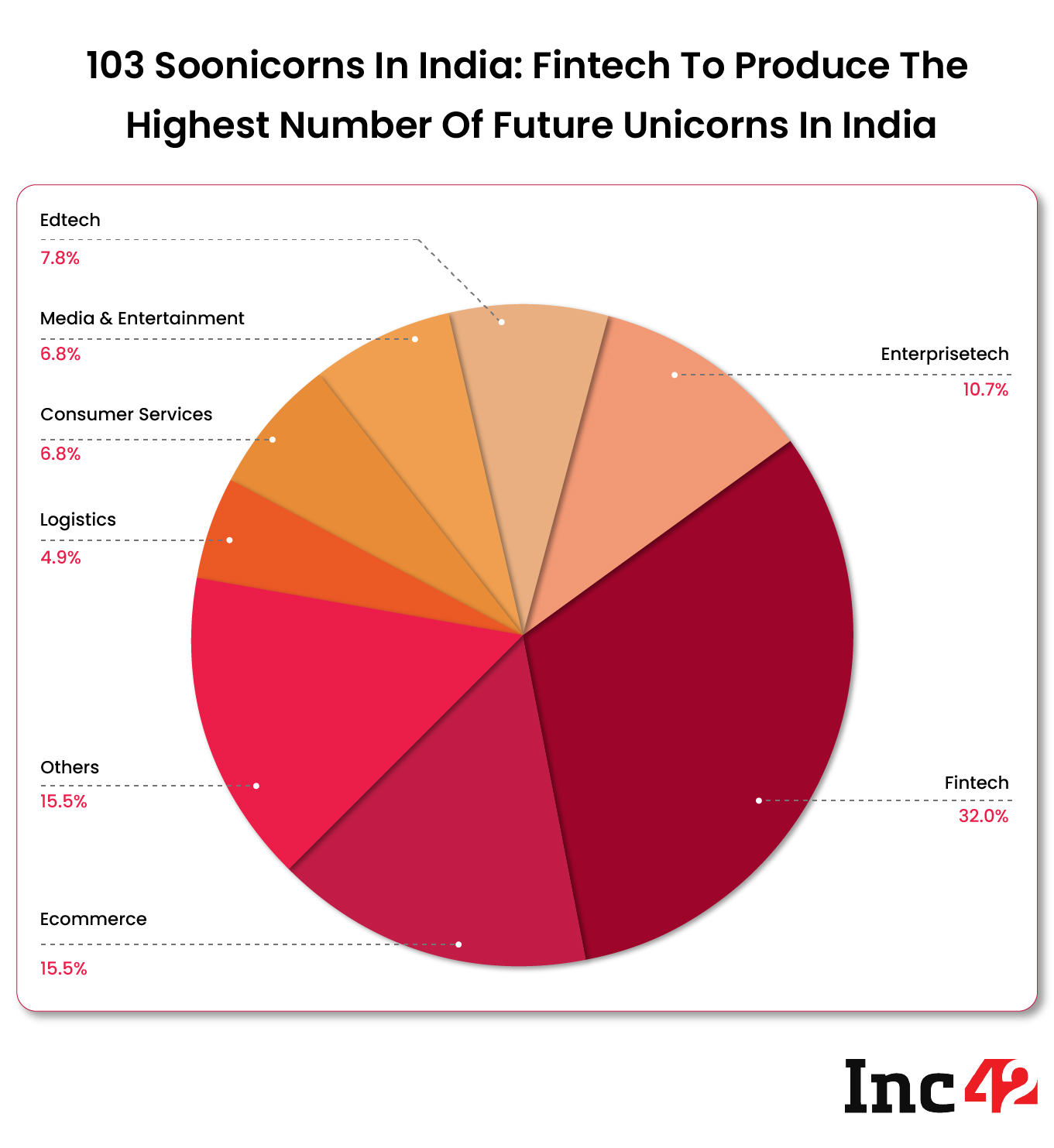

With 33 soonicorns in the segment, fintech is poised to mint the most unicorns over the next few years

Fintech startups have raised $24 Bn in funding between 2014 and Q1 2022, second only to ecommerce

Lendingtech presents the biggest market opportunity by 2025 ($614 Bn), followed by insurtech ($339 Bn) and payments ($208 Bn) within fintech

Fintech is one of the biggest sectors in India’s startup ecosystem in terms of the number of unicorns produced. With 22 of India’s 105 unicorns operating in fintech, the sector is second only to ecommerce in terms of unicorns produced.

According to Inc42’s, ‘The State of Indian Startup Ecosystem Report, 2022’, with 33 soonicorns, the fintech sector is poised to mint most future unicorns in India over the next few years.

India’s startup ecosystem is home to more than 4.2K fintech startups, of which 647 are funded startups. These startups have raised closed to $24 Bn in funding between 2014 and the first half of 2022. Here as well, fintech is second only to ecommerce in terms of funding raised.

Paytm was India’s first fintech unicorn, achieving a $1 Bn valuation in 2015. Since then, the fintech ecosystem has added 21 more unicorns, with 11 being added in 2021. So far this year, there have been four fintech unicorns, with the latest addition being the credit card startup OneCard in July 2022.

The feat is made all the more impressive when one realises that India produced 44 unicorns in 2021 in all. That means that one in every four unicorns made in 2021 was a fintech unicorn.

If the trends in India’s fintech startup ecosystem are anything to go by, then the sector is poised to outdo all others in terms of the number of unicorns made.

Opportunities For Future Fintech Unicorns

Overall, fintech presents a market opportunity of $1.3 Tn by 2025, per an Inc42 report.

Among many subsectors within fintech, lendingtech presents the biggest market opportunity by 2025 ($614 Bn), followed by insurtech ($339 Bn) and payments ($208 Bn). The market opportunity of these three sectors is directly related to the demand-supply gap.

Speaking at Inc42’s Fintech Summit 2022, Nithin Kamath, founder and CEO of investment tech unicorn Zerodha said that lending is one of the biggest opportunities in fintech. “That is a large opportunity; most of the people in the country don’t have sufficient money. How someone will underwrite this risk is a secondary issue, but that is a large TAM,” said the Zerodha CEO.

His point is backed by the fact that credit card penetration in India stands at around 5.55%, per RBI data. This is the reason why lendingtech as a sector is set to grow at a CAGR of 32% between 2021 and 2025. For the likes of Fi, Uni, Lendingkart, Axio, Fino and other lendingtech soonicorns, this might be music to the ears.

With lendingtech, insurtech is also a sector where penetration within India is low and hence, it is the fastest-growing fintech segment in the country.

According to IRDAI data, insurance penetration in India stood at 4.2% in FY21. After the COVID-19 pandemic, insurance spending has increased among people in India, with insurance premiums in the life insurance category expected to reach INR 24 Lakh Cr ($317.98 Bn) by FY31.

The payments market has seen exponential growth since the introduction of UPI in 2016. According to the latest figures from the NPCI, UPI transactions crossed the 6 Bn mark in July 2022. With the upcoming move to link credit cards with UPI, both lendingtech and payments startups are expected to witness a second wind of growth.

Challenges The Future Fintech Unicorns Face

Recently, RBI has been proactive in mitigating risk for the consumer and reining in startups with new policies around credit cards and digital lending, which will force the fintech ecosystem to change business models across the board.

On June 20, the RBI notified that non-bank Prepaid Payment Instruments (PPIs) can’t be loaded with credit lines, effectively putting a break on credit cards from anyone but the banks, sending India’s credit card startups in a frenzy.

The likes of slice had to change their entire business model, going from loading credit lines to adopting a system akin to buy now pay later (BNPL) players. Fintech soonicorns such as Jupiter also had to shut down their prepaid cards business.

Cryptocurrency is a fintech subsector that has been in a regulatory grey area for the past few years. However, that has not stopped the government from implementing a strict taxation regime, with a 30% tax on all gains made on crypto and a 1% TDS, with talks of 28% GST still underway.

The latest norms on digital lending, however, are set to protect customers from lending fraud, extortionate measures for recovery, the steep cost of credit and high-interest rates. The norms also prohibit lending companies from automatically increasing credit limits without the borrower’s explicit consent.

The government is looking to create a fintech environment with the protection of the customer in mind. It is high time fintechs rethink their business strategies to keep the customers’ best interests in mind.

However, in the survey that forms a part of the Inc42’s The State Of Indian Startup Ecosystem Report 2022, 40% of founders were pessimistic about the effectiveness of government policies promoting startups and entrepreneurship. Further, 51% of founders said that abrupt changes in policies hurt the startup ecosystem.

What The Future Holds For Fintech

However, in terms of profitability, fintech startups have lagged. Some of the biggest names in the fintech space remain in the red, with only around a third of India’s fintech unicorns in the black.

Zerodha is one of India’s profitable fintech unicorns, having reported a profit of INR 1,122.30 Cr in FY21. The only other profitable unicorns are Billdesk, MobiKwik, Oxyzo, Chargebee, Razorpay and groww.

Many fintech startups have projected to break even over the next few quarters. Paytm, for instance, has set a September 2023 deadline to break even. However, if profitability does not improve during the next few quarters, consolidation in fintech is set to rise in the face of an ongoing funding slowdown.

Technology such as data analytics, big data, AI and machine learning are set to drive innovation and personalisation will remain a key focus for many fintech startups.

Fintech is one of the most important segments in India’s startup ecosystem, driving innovation in areas which are bogged down by legacy technology and hampered by the unwillingness of people to adopt new technologies.

Areas such as banking, insurance and investment used to be the strongholds of Public Sector Undertakings (PSUs) and large Indian corporates, but India’s fintech startups are rapidly changing the status quo, giving the customers more options to choose from.