A lot is made out of the price of a round.

It’s the one time that, as an investor, I’m not aligned with the founder at all. I want to try to buy up shares of the company as cheaply as possible (and own more) and the founder wants to give up as little of the company as possible.

That all being said, I’ve yet to meet a founder that sold their company for $100 million or more who looks back with great regret at the price they raised their seed round at.

Still, a lot of founders are worried about early dilution and how it affects their eventual outcome when the company is sold. What they may not realize, however, is that a lot of their thinking is tainted by bad mental accounting.

Consider the first money you ever take from VCs. Let’s say you are able to secure $1.5 million from investors. You go back and forth on a price and you eventually settle on a post-money valuation cap of $6.5mm, meaning you have sold about 23% of your company.

It feels like a lot, of course, because you know you’re going to have many more rounds of financing down the line—and if you have to sell 23% every single time you raise money, there’s going to be nothing left very quickly.

At least, that’s how it feels because your brain is doing subtraction. You’re thinking that if you start out with 100% and you lost 23% four times, you’re going to be down to 8%.

In reality, that number is more like 35%.

Hold up.

How do you lose 23% four times, and still own 35%?

That’s because dilution isn’t subtraction. Its multiplication. Every time you sell 23% of your company, you multiply everyone’s ownership by (1 minus 23%.)

And since my ownership is less and less after every round, how much I lose from an absolute percentage standpoint is less and less.

After one round, I own 77.00%.

If I get diluted another 23%, I own 77% x (1-23%), which is 59.29%.

If I get diluted another 23%, I own 59.29% x (1-23%), which is 45.65%.

If I get diluted another 23%, I own 45.65% x (1-23%), which is 35.15%.

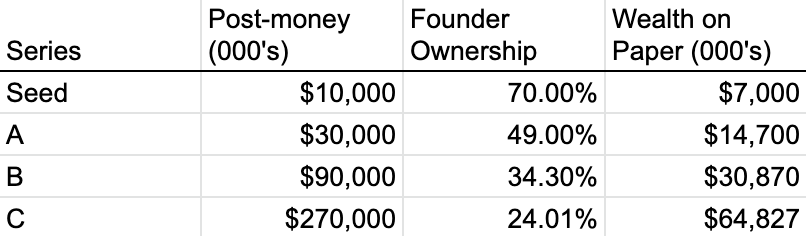

Let’s say the pricing I get on these rounds is worse—way worse—and the amount of dilution I’m taking in each round isn’t 23%, but it’s 30%. The first round is $3mm with a post-money valuation of $10mm, the Series A is $9mm with a post-money valuation of $30mm and so on.

Four rounds later, you’re down to 24.1% ownership, which is less than the 35% you had, but it’s still kind of in the ballpark. Think about that for a moment: Taking 7% extra dilution four times only cost you a cumulative 11% ownership.

Consider the extra padding it could have bought you.

Imagine if every round was 3x the last price—how much did the extra 7% dilution in each round actually buy you in cash?

In the seed round with the $10mm post money valuation, the 7% bought you an extra $700k, going from a $2.3mm round, to a $3mm round. That’s 30% more cash.

In the Series A, that’s $2.1mm, because the round went from $6.9mm to $9mm. The $27mm Series B got bumped up from $20.7 and for the Series C, you tacked on $18.9mm to your $62.1mm round, bringing it to $90mm.

So after four rounds, you could have either raised $92mm and owned 35% of the company, or raised $120mm and owned 24% of the company.

There are, of course, no certainties in the startup world, but if you just took this extra $28mm and stuck it in the bank for a rainy day as you got it, I think there’s a good chance you could ward off the chance that the whole thing blows up and becomes a zero—and that insurance policy seems pretty worth it for 11% after four rounds.

The trippy math part of it is that the extra $28mm that you raised over time, for that extra level of dilution, it’s as if you raised it at a little over a $250mm post-money valuation—because most of the money that came in, buy dollar amount, is coming in much much later, when share prices are higher.

Not convinced yet?

Well, what if I actually started looking at your net worth on paper given those valuations?

This is the smaller piece of a bigger pie theory at work.

There’s pretty much no world in which you’re growing the company’s valuation in a healthy way that you are not getting richer and richer as a founder—it’s not even close to being a bad tradeoff providing you can actually exit at a larger number down the line.

Don’t get me wrong—there are lots and lots of considerations I’m not bringing up here. We’re not talking about the increased bar for a sale that comes with raising money at higher and higher valuations, for example.

And that’s a very good point. The decision to raise or not to raise should be a very serious one that takes into consideration what your eventual outcome will be. If you raise at a higher valuation than you can sell the company for, you could wind up getting crushed by all the equity preference on top of you. Plus, there’s the risk of running in the red for so long that you can’t turn it black should the financing markets shut down on you.

But, that’s another post entirely.

We’re just talking about nitpicking over round-by-round dilution as a way to preserve your ending ownership, and potentially leaving money on the table to do so. With these calculations, it doesn’t seem worth it.

Looking at it another way, the decision to raise another round at all, is a much bigger factor in your ending dilution rather than how much you diluted in each round.

Consider this:

If you raised four rounds of financing at 25% total dilution, you’d be at 32% ownership. If you took one more round at that cost, you’d be at around 24% ownership, a loss of a little less than 8%.

However, if that was a highly competitive round, and you could manage to do it at a 20% dilution, you’d save yourself about 1.5% in ending ownership. Swung the other way, if it cost you 30% of the company to raise that round, you’d lose an additional 1.5%.

That means that 85% of that round’s net dilution to you came in the form of deciding to raise at all, and about 15% of the cost to you came from haggling around the price.

If you want to play with the math, drop your e-mail on this form and I’ll clean up the sheet to make it readable.