Within the startup ecosystem, fintech enjoys a preeminence status. A large number of companies are operating in the fintech space and new players are emerging frequently. It was one of the two top-funded sectors in 2021 as investors were buoyed by the swelling fintech user base and the favourable demography of India. In 2021, fintech startups received close to $8 Bn funding and minted a dozen unicorns.

Industry observers say it is only the beginning of the fintech boom and many startups are reimagining the banking, payment and finance business. The consistent fund flows affirm that fintech in India is a long-term play, according to a market analyst.

The government, meanwhile, has announced that the Reserve Bank of India will soon come up with a digital rupee using blockchain tech. Analysts are confident that the central bank’s digital currency will further boost fintech services.

User Acquisition And Retention Challenge

While fintech space has its own share of obstacles and challenges, customer acquisition and retention is perhaps the biggest challenge for fintech brands.

Since it is a fragmented sector, putting together a customer-first approach is a high priority for these new-age companies. Also, customer loyalty is pivotal because studies have revealed that acquiring a new customer can cost many times more than what it would cost to retain an existing user.

Customers are today spoilt for choices, with new products being launched regularly. This has made finance more complex and customer attention is divided. “The millennials and the Gen Z cohort are managing a disconnected portfolio of providers, apps, virtual cards and banking accounts, which does not result in a seamless experience thus making customer retention more challenging,” said Yashoraj Tyagi, CBO & CTO of CASHe, a fintech company that provides personal loans through a mobile app to salaried millennials.

Cumbersome navigation is what makes a customer desert a particular payment app/mode. Seamless user experience without compromising on data security and privacy is a prerequisite. The very nature of offerings does not give much scope for instant customer gratification and therefore, user retention is particularly challenging for fintech brands.

A simple onboarding process is a key to user retention and acquisition, said Krishnan Vishwanathan, founder and CEO, Kissht, a fintech startup that offers credit at the point of sale. The process needs to be extremely simple and straightforward with minimal clicks and jumps, he said, adding that a delighted customer will continue his engagement.

“Acquisition and retention are key challenges in the digital world because — firstly, there is no direct person-to-person communication with the customer and secondly, the digital mindshare of the customer is minimal. Moreover, with a plethora of easy to transmit communication mediums available, an average customer is inundated with information which often is irrelevant and further shuts off a customer,” he explained.

Understanding the importance of customising communication and engagement at a segment level, Kissht ensures that it sends out relevant information to the customer. It also uses data analytics to understand the propensity to various offers better.

According to Tyagi, staying engaged through regular communication with customers has made a big impact on CASHe’s customer retention efforts. “We have observed that customer satisfaction surveys are a great tool for collecting valuable customer information. By seeking feedback through surveys, we are able to find out what customers really think and feel about our products and services and their overall experiences while using the application for requesting for a loan,” he added.

Further, Vishwanathan said different facets of communications need to be tailored. “We run thousands of concurrent campaigns, each customised to different customers; timing of campaign (morning or evening; weekday or weekend), medium of communication (SMS, IVT, email, notifications, in-app banner), frequency, etc. There is no one size fits all.”

Being simple and direct in all communications and interactions helps because trust is built on the back of simplicity.

CASHe’s customer retention strategies include managing and responding to online reviews. “Learning to respond to negative and positive reviews demonstrates to our existing customers that we care and are listening to what they have to say,” Tyagi said.

It harnesses reviews by broadcasting them on its social media platforms, website. This has helped build a powerful social proof that inspires confidence and fosters customer loyalty. “Also, to nurture customer loyalty, we have built a customer-centric service culture that goes beyond providing transactional convenience. Lastly, staying connected using AI and chatbots to deliver 24/7 support, and acknowledging customers grievances and resolving them within a specific time frame goes a long way in making them feel heard at all times,” Tyagi said.

Martech And Communications To The Rescue

To ensure intelligent engagement and retention of the users, both Vishwanathan and Tyagi use tailor-made, customer-centric solutions provided by full stack customer retention and engagement platform, WebEngage. Similar is the story for alternative debt asset platform Wint Wealth, “We were looking for help to personalise our communications based on the users’ action and WebEngage looked like a right fit,” said Ajinkya Kulkarni, CEO & cofounder of Wint Wealth.

WebEngage, which has over 20 fintech clients in its portfolio, says that it looks to resolve three core issues while working with fintech companies, “Issues because of data silos, issues that have channels silos, and then personalisation. It is a universal problem that lots of folks are facing. These are the core problems that we are set out to solve,” said Minesh Koradia, director, BFSI, WebEngage.

Data Silos

WebEngage offers integration with all the platforms, with a website or an app, or a CRM, or any other systems the client is using, wherever customer data is residing. According to Koradia, once the data bit is taken care of, engagement is an easy problem to solve. “You can plan and strategize your engagement based on the data you have, the sort of segments that you want to create, or the type of analytical finance that you want to create,” he explained.

Channel Silos

Fintech brands have been facing the issue of channel silos. WebEngage provides all the channels under one roof under one umbrella which helps in a big way. “Our platform is so open that they can kind of bring in their own partners or they can use our preferred partners for communication requirements. Doing one-to-one communication is the third issue,” said Koradia.

Once data is resolved, one-to-one communication using variables or core attributes or behaviour-based attributes is easy to implement in campaign strategies.

Significance Of Omnichannel

“I think, slowly and steadily, people are realising that omnichannel is the way to go. Because it will not just help them know, give better customer experiences it also helps them optimise their communication strategies, optimise the communication costs,” said Koradia.

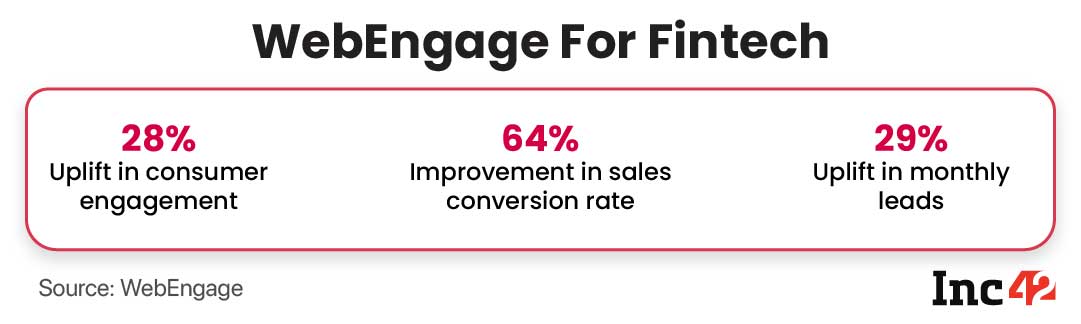

WebEngage Impact For Indian Fintechs

Wint Wealth’s Kulkarni speaks highly of WebEngage’s journey feature, “It is very simple and intuitive to use and helps us automate our communications at various touchpoints of the user to achieve a target.” Also, the impact analysis available on the campaign level helps in learning what works, he added.

Through the Journey Builder feature, data-backed, hyper-personalised campaigns could be created at scale resulting in a 300% increase in CASHe’s loan disbursal value, Tyagi said, adding that WebEngage helped CASHe reduce human hours by 75%. It was automation of the user engagement initiative that made it possible.

“In addition to the increase in new disbursals, we have been able to scale up our repeat disbursals with 40% of our user base requesting a second loan within 24 hours of closing their first loan,” Tyagi said.

Wint Wealth grew from 15K users to over 1 Lakh users since it started WebEngage. “This Journey Design feature helped us with engaging users in the best way,” said Kulkarni.

For a player like Kishht that runs multiple campaigns manually targeting over 10,000 customers on a daily basis, it was cumbersome and prone to errors and delays. WebEngage has allowed Kissht to easily and seamlessly keep the customers active and engaged. Says Vishwanathan: “The flexibility with segmentation as well as creating very complex but powerful communication flows on the same — this has been an absolute game changer and real problem solver for us.”

This has allowed Kissht to drastically improve its funnel performance and reduce drop off rates by over 40%.

Future Of The Indian Fintech Revolution

According to Inc42’s State Of Indian Fintech Report, Q1 2022, in three years — by 2025 — India’s overall fintech market opportunity is estimated to be $1.3 Tn, growing at a CAGR of 31% between 2021-2025.

According to Tyagi, in the immediate term BNPL and Neobank models will likely be the flag bearers of the financial revolution in India. The main challenge will be the dynamic nature of regulatory reforms, which will have a cost-related impact on users and businesses.

“Neobanks will provide a more diversified one-stop solution to over 17 Mn citizens by 2026, with virtual cards being the latest among the ingenious solutions on offer. Similarly, the credit sector also continues to evolve, with BNPL models taking the centre stage and slated to become a $56-Bn sector by FY26,” Tyagi said.

According to Vishwanathan, open-source banking (open banking or neobanks) will provide fintech participants, who are otherwise payments first or credit first, an opportunity to offer a full bouquet of offering to customers.

As digitisation is likely to grow at a good pace, one area where penetration potential is significant is small establishments. Vishwanathan noted that in small kirana stores, tea/food vendors, vegetable sellers, etc. About 75% of transactions are still in cash. “These will afford opportunities on payments and credits in a significant manner. Small business owners are a key segment for us and we plan to significantly enhance our credit offering for the same,” he said.

Thanks to the digital infrastructure comprising Aadhaar, UPI and GST, the Indian fintech industry is already the third-largest in the world. Experts said probably the time has come for some brands to foray into foreign geographies — while Paytm has already made the move by partnering with SoftBank and Yahoo Japan to launch its arm PayPay in Japan back in 2018.

As the fintech space is on the cusp of phenomenal growth, collaborations with financial institutions will be the key differentiator. But the success will hinge on strategic choice partnership models.

![Read more about the article [Funding alert] Oye Rickshaw raises Rs 24 Cr from Alteria Capital to expand EV energy infra](https://blog.digitalsevaa.com/wp-content/uploads/2021/03/V-05-1600852077699-300x150.png)