RBI’s policy barring NBFCs from lending through PPI threatens to disrupt well-funded fintech startups

The best policies, laws and regulations in the world are lauded for being future-proof. Unfortunately for policymakers, regulating technology is like swimming against the current — just ask the Indian fintech ecosystem this week.

While the mood of the fintech sector was lifted earlier this month with the move to link credit cards to UPI, now we can note quite a few crests falling. The RBI’s policy to bar NBFC lenders from PPI credit instruments threatens to disrupt a slew of well-funded fintech startups in India.

Before we dive into the potential implications of this and other recent changes for the fintech sector, let’s take a look at the top stories this week:

RBI Vs Fintech Startups

It’s no secret that India’s fintech sector has had major issues with the revenue model thanks to the zero MDR regime for UPI, the flagship digital payments platform. And beyond payments, growth in other fintech subsectors is largely dependent on marketing spends — as seen in the case of insurance tech, BNPL or other neobanking ads.

Sustainable growth is not a hallmark of this sector, and that’s why when regulations come, they often threaten to disrupt swathes of the market. Which is what RBI’s notification on PPIs working with NBFCs for credit line instruments and products has done for the lending tech segment.

It’s also eliminating some of the grey areas in which startups had operated with NBFCs to ease access to loans, which have also caused issues such as harassment and aggressive recovery methods.

RBI Disrupts Fintech’s Last Hope?

In the absence of real revenue from payments or neobanking, most startups in this space have added lending and BNPL as a feature to attract users, including unicorns such as Paytm, PhonePe, MobiKwik and others. Given the lack of banking penetration in India and the lack of credit history among customers, startups were filling the gap and for a while, it was as easy as submitting a video KYC for just about anyone to get a loan in India.

The biggest fear for the RBI is the possibility of a debt trap for consumers and merchants, who have been given credit without much risk assessment.

While many fintech companies partner with banks to issue cards and digital wallet instruments, loans or BNPL are tacked on to the card. The credit lines associated with these cards are backed by NBFCs, a practice that the RBI is trying to eliminate.

The use of NBFCs for credit lines on PPIs was not explicitly barred by the RBI thus far, so startups were operating in a grey area.

Startups such as Slice, OneCard, Jupiter, Uni, ZestMoney and KreditBee have long used their PPI licences to issue payments cards or wallets, and then add credit lines to these cards. Amazon Pay, Paytm Postpaid and Ola Money are likely to be impacted as well depending on how much of their loan book is driven by such routing.

“We believe this regulation could significantly impact the fintechs involved in this business and would be advantageous to banks, as they can further accelerate card acquisition with less competition,” brokerage firm Macquarie said about the RBI ruling.

Will The Credit Tap Dry Up?

Currently, there’s no clarity on how much of an impact it will have in terms of the lending value, because there’s no transparency on how much credit has been offered through this route.

“All digital lenders borrow funds from RBI authorised entities and RBI has a clear trail to identify the transactions. However, with the involvement of prepaid instruments as a credit option through NBFCs, keeping everything under RBI purview has become difficult,” the founder of a digital lending startup told Inc42 on the condition of anonymity.

Fintech lenders may move to PPIs through banks and continue to offer their services within the purview of RBI guidelines, but this is likely to cause a rush for access to capital from banks, and give banks more leverage in the process.

India Mimicking China

RBI’s move has shades of what China did to lending startups and fintech giants last year. As reported in The Economist, China’s crackdown on fintech companies was largely an effort to limit the influence of giants such as Ant Financials, break up monopolies in the fintech ecosystem, give banks a bigger chunk of the market and get access to private customer data.

In India’s case, thus far, there’s been no explanation from the RBI on why it has taken this step. So while there is no direct comparison with China, it’s still a move that damages fintech growth. For instance, former BharatPe founder and MD Ashneer Grover said RBI’s move is aimed at protecting the credit card business of banks.

As Macquarie added in its report, the RBI has not been keen on digital banking licences thus far and has called for tighter regulations in the past year or so. So the message is that fintech companies will be regulated more and more closely. “It is clear to us that the risks are increasing for the fintech sector, for which regulations have been a light touch so far,” the firm added.

The fintech opportunity in India is estimated to reach $1.3 Tn by 2025, growing at a CAGR of 31%. And today, India has 21 fintech unicorns and more than 4.2K+ active fintech startups. Tight regulations run the risk of devaluing many of these startups with, and also spooking investors in the process.

Are Regulations Killing Innovation?

In private, startup founders are questioning why entities that follow KYC norms and other RBI guidelines have to keep going through such disruptions every few months.

Whether it is the UPI transaction cap or the utter confusion in the crypto industry, startups feel that innovation cannot happen with such changing financial regulations. Jupiter and KreditBee have temporarily stopped customers from transacting with their cards.

Founders told us their focus needs to be on product building and creating impact in terms of financial inclusion, not on compliance. Such sudden decisions can have a negative impact on investor sentiments, and any companies whose funding is stalled might have to cut costs or lay off employees.

Ultimately, while all players are more than happy to comply with regulations, the biggest complaint is that regulations are often thrown into the mix without any warning. They tend to blindside founders and startups, which is what the RBI and other regulators have repeatedly done.

While right now fintech startups and industry bodies have sought an extension to comply with the new norms for lending through PPI, there’s no telling whether the RBI will see their side of the story.

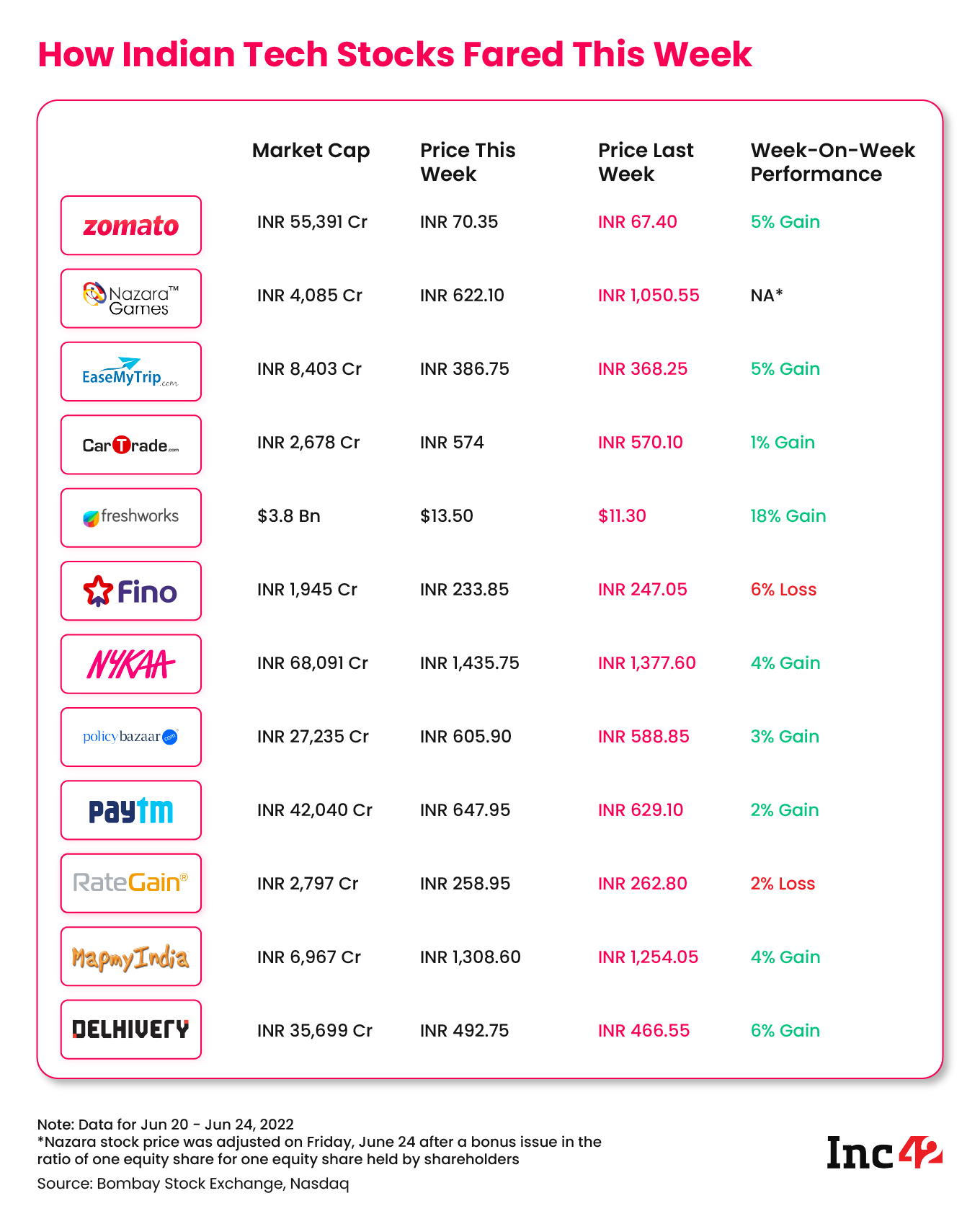

Tech Stocks & Startup IPO Tracker

Here’s how the past week has been for the listed tech companies we are tracking:

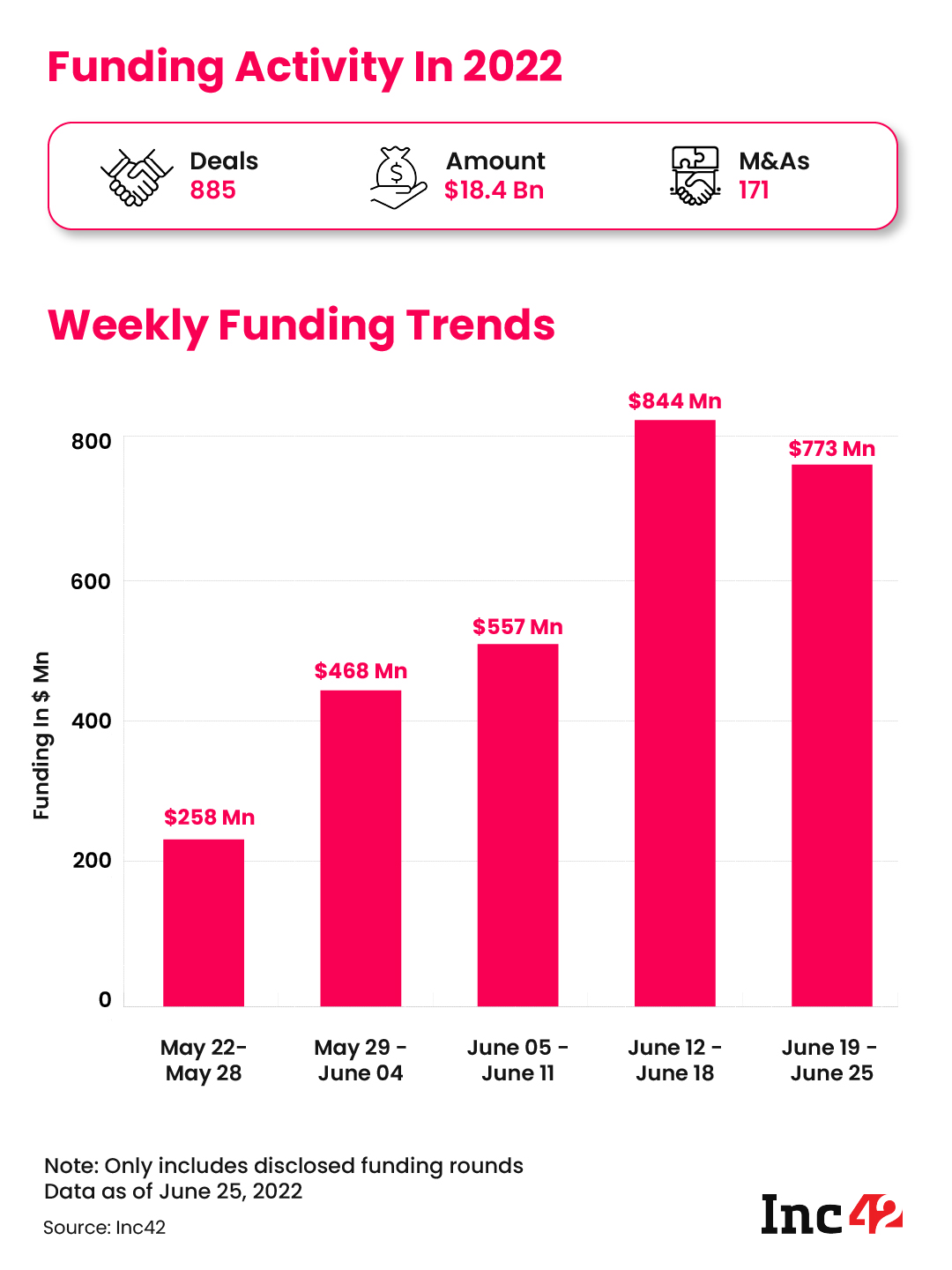

Startup Funding Tracker

- New Unicorn: SaaS startup LeadSquared entered the unicorn club with a $153 Mn round led by Uncorrelated Ventures, Fasanara Capital and Abstract Ventures

- Funding Roundup: This past week, the Indian startup ecosystem raised funding to the tune of $791 Mn across 27 deals, with Stashfin’s $275 Mn Series C round being the largest deal

Influencer Tax & Other Top Stories

- Ola’s Experiments End: Ola has decided to shut down used cars marketplace Ola Cars and quick commerce business Ola Dash to focus on EVs and the mobility biz

- Influencer Tax: Social media influencers in India who get free merchandise for sales promotions now have to pay a 10% tax on such benefits

- Matrix’s New Fund: The Indian arm of US-based Matrix Partners is looking to raise a $450 Mn fund after last closing a fund in 2019.

- Zomato’s Blinkit Deal: While Ola is exiting quick commerce, Zomato is doubling down with an INR 4,447 Cr all-stock deal to fully acquire Blinkit

- Travel Wars: After Meesho, publicly-listed EaseMyTrip is the latest company to consider legal action against an online smear campaign run by unknown persons

That’s all for this week. We will see you next Sunday with another weekly roundup.

![Read more about the article [Funding alert] Women skilling and employment platform WiT-ACE raises $1M in seed round led by founders of Cit](https://blog.digitalsevaa.com/wp-content/uploads/2021/03/funding-1615270729201-300x150.png)

![Read more about the article [Startup Bharat] How Surat-based Canvaloop is making conscious effort to develop eco-friendly fibres](https://blog.digitalsevaa.com/wp-content/uploads/2021/12/canvaloopfinal-1638464239003-300x150.png)