Jack Selby wears many hats. He is a film producer, with movies like Freeheld and Act of Valor under his belt, and a well-respected venture capitalist in Silicon Valley. He is also part of the “PayPal mafia”—former executives at the payments giant who later went on to back other tech companies.

But perhaps Selby’s most prominent role is that of managing director at Thiel Capital—the family office of tech visionary and former CEO of PayPal, Peter Thiel.

Thiel, who was the first big investor in Facebook (now Meta), has also backed startups such as Stripe and Elon Musk’s SpaceX. Thiel Capital backs more than 15 startups worldwide including Alloy Therapeutics, QA Wolf and Wild Earth.

Speaking to YourStory on the sidelines of the TiE Global Summit 2023 and Singapore Fintech Fest, Selby deconstructs hype cycles in the funding ecosystem and tells us why he is bullish about India.

<figure class="image embed" contenteditable="false" data-id="532248" data-url="https://images.yourstory.com/cs/2/f3638ff0dcc111ec93bca187955479ef/JackSelbyInterviewQuote1-1701704603870.jpg" data-alt="Jack Selby Thiel Capital" data-caption="

Infographic by Nihar Apte

” align=”center”> Infographic by Nihar Apte

Edited excerpts:

YS: Thiel Capital started investing heavily in China back when it was still emerging years ago. What about the country stood out for you?

Jack Selby (JS): As part of the investment thesis for our macro hedge fund, we looked closely at both India and China ten years ago. Without meaning any offense to India, China at the time seemed like a more important macro country just in terms of how well it fit in with the other players globally.

I visited China every month for the next three to four years and was left exceptionally impressed with everything taking place on the ground—right from the quality of entrepreneurs to truly unique innovations. They were far from building copycat companies and had this frenetic energy in the air 24/7.

But, now we have been locked out given the geopolitical situation. It’s a pity.

YS: What is your take on the current Indian startup landscape?

(JS): Even though we opted to bet on China ten years ago, I am just as bullish about India today. It has immense potential to grow especially if the opportunities are realised to the fullest extent by the people present on the ground.

Making good use of local networks as well as raising adequate capital from the right people could be a differentiating factor for those wanting to build out of India.

India probably has the best growth story in the world. China has a great growth story too but it’s not as open a market anymore.

YS: If you could go back in time and re-evaluate your decision to invest in China, would you change your mind?

JS: Maybe, if I had known the geopolitical situation would turn out the way it did. But that was impossible to know. So I’m not sure.

Moreover, China is a bit closer to the US so the decision was slightly easier. (laughs)

But it’s not too late to enter India. Both India and China have a century plus to go. So if one hasn’t been in the game so far—like we say in baseball—they would have missed the first or the second innings, but there’s still a lot left in the game to play.

YS: It has been a tough couple of years for startups around the world in terms of securing capital. You have been observing the situation closely, how bad is it?

JS: You know, after the great financial crisis when interest rates were zero effectively, money was so easy-flowing. Without naming names, there were these bunch of investment funds that raised a ton of money and then started parachuting around the world, writing crazy cheques at crazy valuations between 2019 and 2021.

These funds parachuted into India as well and created a big pool of tourist capital and spent two years writing so many stupid cheques. Soon enough, they realised that they needed to go back home to tender their gardens and clean up the mess. This is why these funds are not showing up in India anymore.

The triage process is going to be painful and is going to fully occupy their (the investment funds) time going forward.

<figure class="image embed" contenteditable="false" data-id="532251" data-url="https://images.yourstory.com/cs/2/f3638ff0dcc111ec93bca187955479ef/JackSelbyInterviewQuote21-1701704989186.jpg" data-alt="Jack Selby Thiel Capital" data-caption="

Infographic by Nihar Apte

” align=”center”> Infographic by Nihar Apte

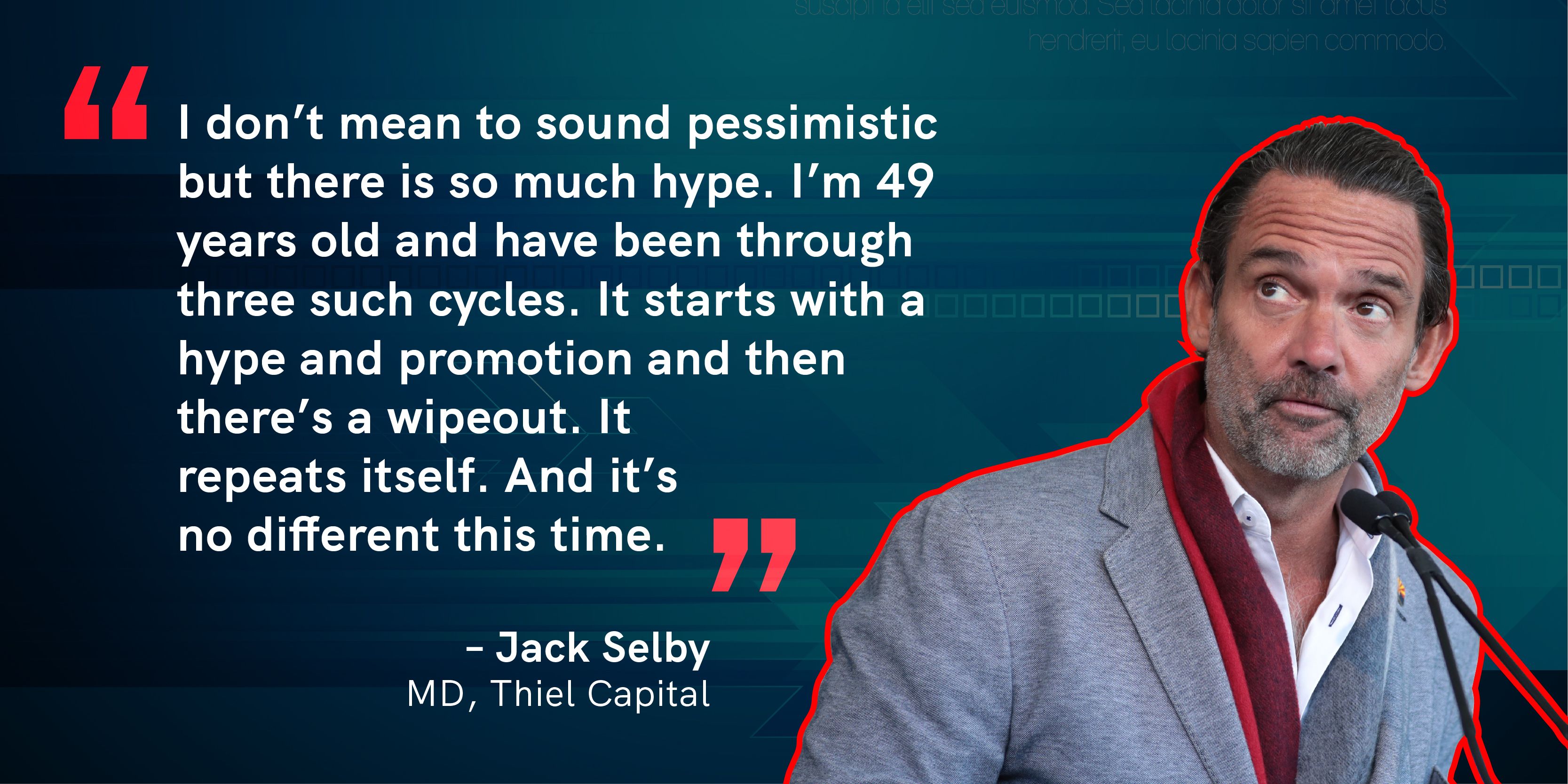

YS: You sound quite pessimistic about the situation…

JS: I don’t mean to sound pessimistic but there is so much hype. I’m 49 years old and have been through three such cycles. It starts with a hype and promotion and then there’s a wipeout. It repeats itself. And it’s no different this time.

For the sake of young entrepreneurs and audiences, we’re just trying to bring about balance more than anything else because raising money is really, really, really hard right now.

Especially if one is running a capital expenditure (capex) intensive business and has not raised a single penny in the last 13 years, they’re certainly not going to get funded now; which means that sector will get wiped out.

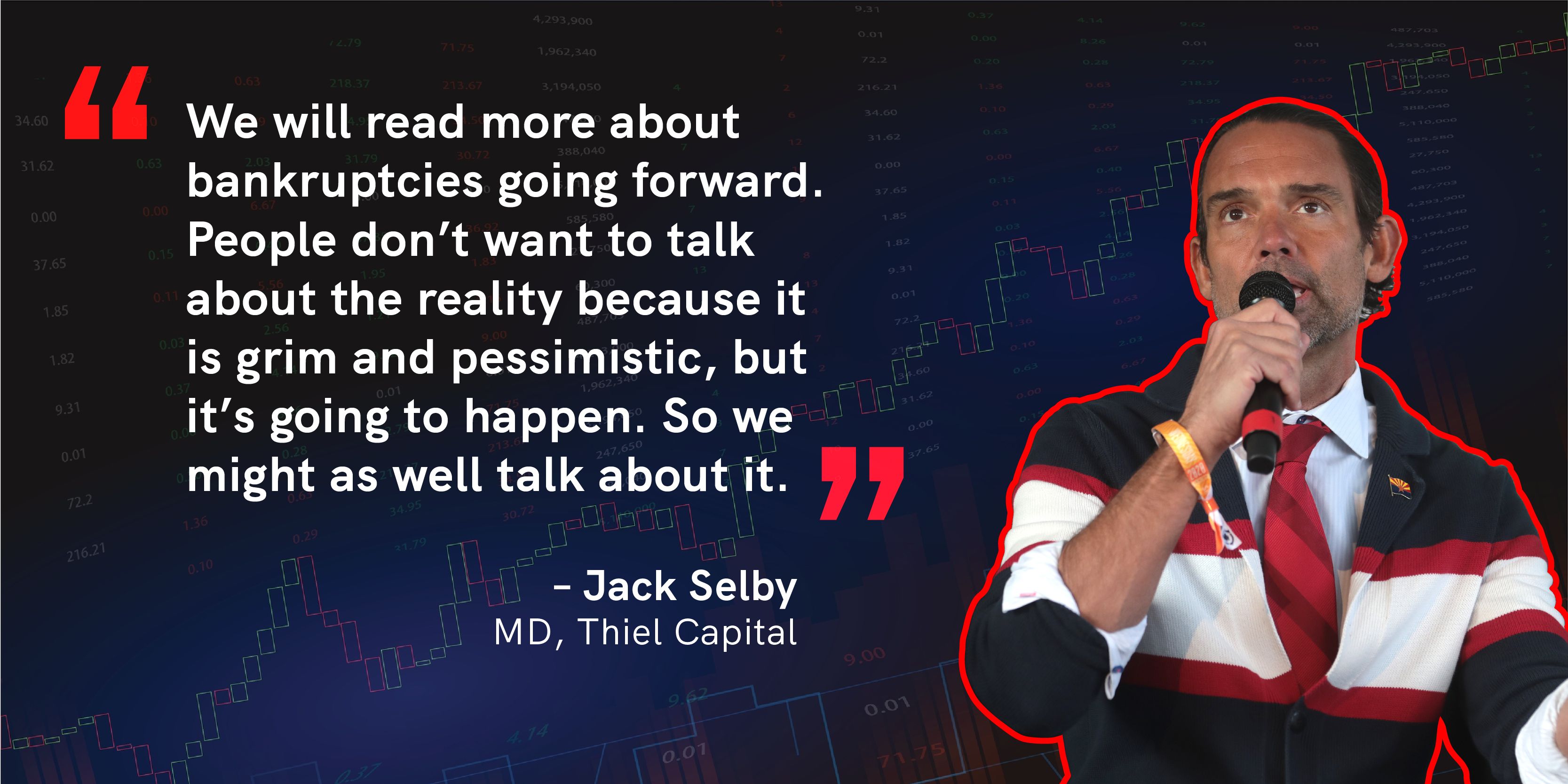

We will read more about bankruptcies going forward. People don’t want to talk about the reality because it is grim and pessimistic, but it’s going to happen. So we might as well talk about it.

YS: What kind of businesses are more likely to go bust during this down time?

JS: We have already started reading about companies that are truly not viable. For instance, there are some companies started by Hollywood celebrities that are obviously going to go bankrupt in the near future.

Specifically, capex-heavy businesses will have it tougher than the others. The collapse of Convoy—the Seattle-based supply chain startup that was once valued at $3.8 billion and funded by Microsoft’s Bill Gates and Amazon’s Jeff Bezos—is the biggest global example of the future we are staring at.

I argue that there will be at least one Convoy-equivalent in every sector while some sectors will see many Convoys. It’s a question of when not if. If one’s business model relies heavily on capex spending, there’s no magic wand.

For the ones that do survive, the recovery will essentially be U-shaped and not V-shaped because these companies are likely to have so much cash that it buys them an opportunity to try to figure out survival.

<figure class="image embed" contenteditable="false" data-id="532247" data-url="https://images.yourstory.com/cs/2/f3638ff0dcc111ec93bca187955479ef/JackSelbyInterviewQuote3-1701704507397.jpg" data-alt="Jack Selby Thiel Capital" data-caption="

Infographic by Nihar Apte

” align=”center”> Infographic by Nihar Apte

YS: Which sector excites you the most?

JS: This question gets asked a lot and I always shake my head, because honestly, I don’t think anyone knows. I don’t think Peter (Thiel) knows. I don’t think Elon (Musk) knows. I don’t think even the Pope knows.

However, one of the things that Peter always says is that the more buzzwords an investment deck has, the worse the company usually is. So the overuse of words like blockchain, artificial intelligence (AI), etc are generally not good indicators.

I was fortunate enough to have worked with a talented group of people when we started PayPal 20 plus years ago and I have witnessed the investors investing in people and their progeny. This has helped me become sector agnostic.

I joke that I’m a liberal arts major and a major in economics and I can wrap my head around most things. But if it’s domain-specific—like biotech—that’s way above my head and I’m probably going to pass. Simply understanding the opportunity makes a difference.

YS: Do you think India has any advantage over other countries in terms of navigating the challenging period?

JS: The good news is that the tourist investors that showed up in parachutes half a decade ago, are not showing up anymore. Businesses in India no longer have to compete for foreign tourist capital.

At the end of the day, the people that should capture the value are the people who are on the ground and those who know the ones growing these companies. The best thing that can happen to any emerging ecosystem is to witness the influx of resources, have the participants push the chips back in, recycle it, and go for the next goal. It’s harder to do so when the money is coming from outside the country.

The fact that the money has now been forced to go home means that predominantly local investors will take up the baton. I think it will give the ecosystem the ability to maintain the dynamic of pushing the chips back into the table and getting the snowball effect rolling.

<figure class="image embed" contenteditable="false" data-id="532249" data-url="https://images.yourstory.com/cs/2/f3638ff0dcc111ec93bca187955479ef/JackSelbyInterviewQuote4-1701704706668.jpg" data-alt="Jack Selby Thiel Capital" data-caption="

Infographic by Nihar Apte

” align=”center”> Infographic by Nihar Apte

YS: Easy money resulted in hyper valuations. Is it as bad in India as in the rest of the world?

JS: Like I said earlier, India and China have great growth stories and it’s not too late for investors to focus on these two countries.

I think the entry point into India has become easier and more lucrative now since the cycle has turned. This is mostly because valuations in India are much better now, contrary to the time when money was so easy and everyone wanted to be an entrepreneur. It was harder for folks on my side of the table to tell who is genuine and in the game for the right reasons from those who were playing the game because they wanted to be a millionaire.

The second set of people have returned home to do what they were doing before which made the process of culling the herd that much more efficient.

YS: Corporate governance in startups seems to have become a pressing discussion in boardrooms today. How do you typically approach the topic?

JS: When the ecosystem enters into a frothy momentum market, core components like fiduciary responsibility no longer remain the primary consideration. Unfortunately, it is human psychology to allow the responsibility to fall by the wayside more than it should when one gets caught up in the frenzy.

However, the cycle has now turned and is forcing investors to roll up their sleeves and evaluate their portfolio to figure out which companies would survive and which wouldn’t. That’s the hard part of the job. But it is what they get paid to do and I think it’s healthy.

Like I said, it’s just cycles; we’ve seen it before and it’s not any different this time. When it’s frothy, things go bust, people come in, and clean up the mess. They remember their fiduciary responsibilities that they may have forgotten during the boom times. It ebbs and flows and is a natural part of the cycle.

In the Indian context, it is important to appreciate the cultural uniqueness of the different places one is investing in. Too many western investors have in the past used the prism of western investing and blindly applied it to India to spot something amiss. It was not necessarily the case and so it’s unfair.

<figure class="image embed" contenteditable="false" data-id="532250" data-url="https://images.yourstory.com/cs/2/f3638ff0dcc111ec93bca187955479ef/JackSelbyInterviewQuote51-1701704777918.jpg" data-alt="Jack Selby Thiel Capital" data-caption="

Infographic by Nihar Apte

” align=”center”> Infographic by Nihar Apte

YS: You launched a $110 million fund last year to invest in startups emerging out of your hometown in Arizona. What motivated the decision?

JS: Over the years, I have spent a lot of time thinking about how to build tech ecosystems outside of the traditional hubs. I lived in the state of Arizona for more than 20 years and noticed that even though it was a population centre and had great educational resources, it lacked capital. Some of the best entrepreneurs would go to Colorado, Utah, and California to get funded.

Once the money comes in from someplace far away, there will be some sort of gravitational pull to spend more time where the cheque was written. For instance, say a Salt Lake City venture capitalist ploughs money into a startup from Phoenix which ends with a huge outcome like a public offering, the proceeds will largely go to the person sitting in Salt Lake City who will push the chips back into the Salt Lake City ecosystem, and not into the Phoenix ecosystem.

The idea of the fund was to encourage the recycling of expertise and outcomes.

YS: Do you think the same principles could be applied to driving the startup ecosystem in India’s Tier II and Tier III cities as well?

JS: Certainly. India has the population centre, amazing universities, and plenty of capital. We’ll just have to give businesses their own time to make successful outcomes. Once that is achieved, there is a need to ensure the outcome gets recycled and retained within the boundaries of the country.

The Arizona fund was by far the hardest fundraise I have ever done, and I’ve done many. The idea was to get as many Arizona locals to put in money so that they have a say in how the money is being deployed. One of the main reasons why the locals were willing to invest in the fund was because they wanted to see their child graduate from a local university and have access to diverse employment opportunities within the state.

This would strike a chord with the Indian diaspora, in that sense, since there are Indians all over the world and if they can be captured and kept close to home, one could certainly say that it’s a successful outcome.

(Lead image source: TiE Singapore; redesign by Nihar Apte)

Edited by Jarshad NK

![Read more about the article [Startup Bharat] These students from Indore are building low-cost trendy furniture using plastic waste](https://blog.digitalsevaa.com/wp-content/uploads/2021/05/IMG-23792-1620901668128-300x150.jpg)

![Read more about the article [Funding alert] Sedai raises $15M in Series A; plans to open R&D centre in Kerala](https://blog.digitalsevaa.com/wp-content/uploads/2022/03/ImagesFrames22-1647404890998-300x150.png)